The Rise of the 50-Year Mortgage: Could It Be the Future of Homeownership?

As housing prices continue to climb in many parts of the world, policymakers and lenders are exploring new ways to make homeownership more accessible. One idea gaining attention is the 50-year mortgage — an ultra-long-term home loan that stretches payments over half a century. While this concept isn’t entirely new, renewed discussions about affordability and intergenerational housing are bringing it back into the spotlight.

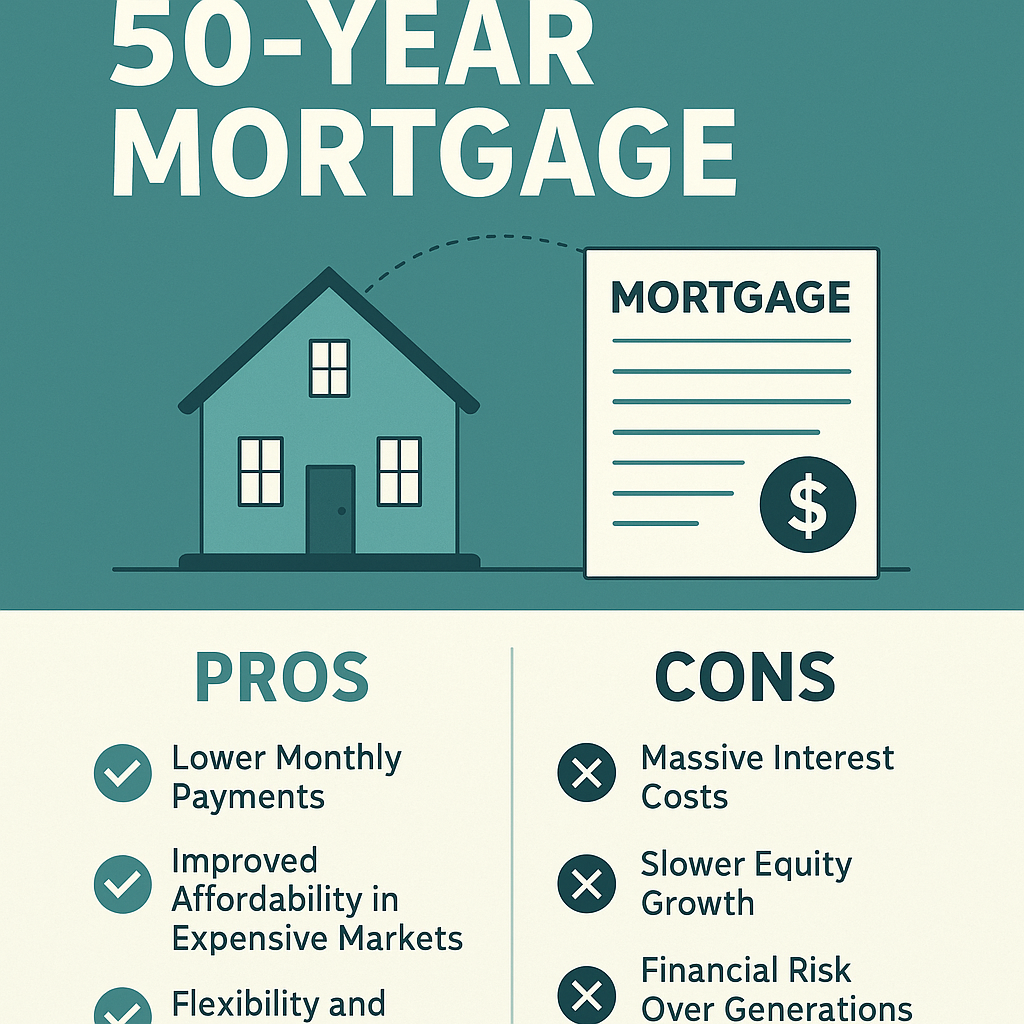

What Is a 50-Year Mortgage?

A 50-year mortgage is an extended-term home loan that allows borrowers to repay over 600 months, compared to the more traditional 30-year period. The main appeal lies in lower monthly payments, which can help first-time buyers or those in high-cost cities qualify for larger loans.

However, this comes at a cost — notably more interest paid over time and slower equity growth.

The Potential Benefits

1. Lower Monthly Payments

By spreading payments over 50 years, borrowers can reduce their monthly financial burden. This could make homeownership accessible to those who might otherwise be priced out.

2. Improved Affordability in Expensive Markets

In cities like San Francisco, Toronto, or London, where home prices can exceed $1 million, a 50-year term can make the difference between renting indefinitely and owning a home.

3. Flexibility and Cash Flow

Lower payments can free up funds for other investments, education, or retirement savings. For younger buyers, this flexibility might outweigh the long-term cost.

The Drawbacks and Risks

1. Massive Interest Costs

A longer term means paying significantly more interest, sometimes hundreds of thousands of dollars extra, compared to a 30-year mortgage.

2. Slower Equity Growth

Because a larger share of early payments goes toward interest, homeowners build equity very slowly. This could limit refinancing options or reduce financial security later.

3. Financial Risk Over Generations

A 50-year term means some borrowers may still be paying their mortgage into retirement — or even pass the debt to heirs. That introduces a new kind of intergenerational financial dependency.

4. Market and Inflation Risks

Over the past five decades, interest rates, inflation, and property values have fluctuated wildly. Predicting long-term affordability is nearly impossible.

Would It Work in Practice?

Countries like Japan and the UK have experimented with ultra-long mortgages, sometimes allowing multi-generational loans where children inherit both the home and the remaining mortgage. While this model can make sense in stable, high-value markets, it also raises ethical and financial questions: should homeownership really take a lifetime — or more?

A Balanced Perspective

The 50-year mortgage could become a tool for improving housing access, but it is not a universal solution. For some, it could offer breathing room; for others, it could trap them in a long-term cycle of debt. The key is responsible lending, transparent interest structures, and strong consumer protections.

Final Thoughts

A 50-year mortgage reflects both innovation and desperation in the face of a housing affordability crisis. It challenges the traditional idea that a mortgage should be paid off within one lifetime. Whether it becomes mainstream will depend on how society balances immediate affordability against long-term financial well-being.